24-HR Emergency Service: 1-800-300-4875

24-HR Emergency Service: 1-800-300-4875

August 17, 2022

The controversial $740 billion partisan budget reconciliation package, the Inflation Reduction Act of 2022, was signed into law by President Biden on Aug. 16 following its passage by the U.S. Senate on Aug. 8 (51-50) and the U.S. House of Representatives on Aug. 12 (220-207).

Ahead of the bill’s Senate passage, ABC issued a statement opposing the IRA, an ABC grassroots action alert and a key vote letter to the Senate against the bill. ABC also issued a statement reacting to Senate and House passage of the bill.

ABC joined a coalition of small business organizations in opposing the legislation’s harmful tax provisions, which are highlighted in this ABC analysis of the IRA’s troubling tax hikes and restrictive labor policies.

Problematic language in Subtitle D-Energy Security of the IRA generally slashes longstanding and current clean energy tax credits from 30% to a baseline credit of 6%. However, the IRA gives developers a bonus tax credit that is 500% higher than the baseline credit if they require project contractors to pay construction workers union-scale, government-determined hourly wages and benefits via the archaic and inflationary Davis-Bacon Act of 1931 and use apprentices enrolled in government-registered apprenticeship programs. In most cases, both conditions must be met to qualify for the bonus rate.

Rewriting the U.S. tax code to enact pro-labor policies sets a dangerous precedent that rewards special interests and distorts the free market’s compensation and workforce development practices on private construction projects. This new bonus credit not only penalizes employers that believe in fair and open competition and pay wages based on experience, quality and market rates, but also limits opportunities for thousands of small businesses, construction workers and industry-recognized apprentices.

The following ABC assessment of the IRA’s new labor requirements on clean energy and energy efficient commercial buildings (179D tax deduction) construction projects eligible for these tax credits may evolve following additional clarification and forthcoming rulemaking.

Prevailing Wage Requirements for Bonus Credit on Eligible Projects

Developers seeking the full bonus credit must require contractors and subcontractors to pay laborers and mechanics employed for the construction and alteration or repair of a qualifying project an hourly prevailing wage rate set by the U.S. Department of Labor via the Davis-Bacon Act.

In the event developers fail to satisfy these requirements, the developer may cure the discrepancy—and thus still claim credits at the bonus rate—by compensating each worker the difference between actual wages paid and the prevailing wage, plus interest, in addition to paying a $5,000 penalty to the U.S. Department of the Treasury for each worker paid below the prevailing wage during the taxable year.

If the U.S. Treasury secretary determines that the discrepancy is the product of intentional disregard, the developer must compensate each worker three times the difference in wages and the penalty to the Treasury is increased to $10,000 per worker. Once the secretary determines that a discrepancy occurred, the taxpayer must make payments to the employees and the Treasury within 180 days of the determination in order to remain in compliance with the prevailing wage requirements.

Of note, non-compliance penalties appear to differ from those currently set under long-standing requirements of the Davis-Bacon Act, as the DOL’s 2022 proposal making radical changes to Davis-Bacon Act regulations is expected to create additional confusion and uncertainty for stakeholders.

Forthcoming regulatory guidance from the Treasury for the IRA and the DOL for new DBA regulations may provide additional clarity. Expect analysis from ABC following the release of this information.

Government-Registered Apprenticeship Requirements for Bonus Credit on Eligible Projects

Developers of qualifying projects are required to use apprentices from government-registered apprenticeship programs for 2024 for at least 15% of the total labor hours of the project, which phases in at 10% for construction work beginning in 2022, 12.5% for construction work in 2023 and 15% in 2024 and thereafter.

Each contractor and subcontractor employing four or more individuals on a qualifying project must employ one or more apprentices from a government-registered apprenticeship program.

The project must follow applicable apprentice-to-journeyperson ratios for each trade, as specified by the DOL or equivalent state agency.

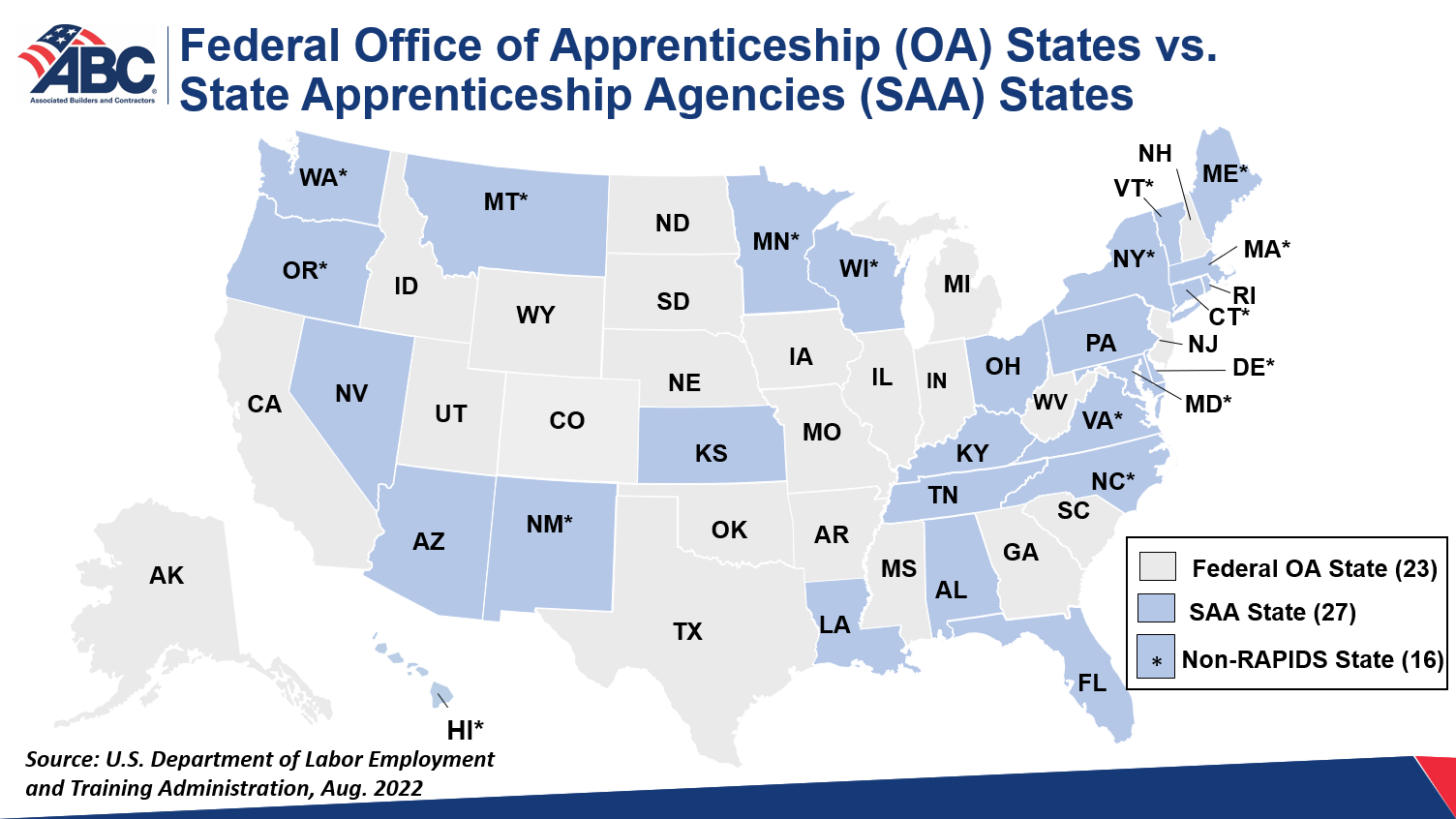

Of note, government-registered apprenticeship programs may not have the capacity to meet these demands, as there are few GRAPs in some states and they graduate only 40,000 to 45,000 construction industry apprentices a year, as discussed here.

In the event a developer fails to satisfy these requirements, the developer may cure the discrepancy by paying a penalty to the Treasury equal to $50 multiplied by the total labor hours for which the requirements are not satisfied. This penalty is increased to $500 per hour in the event the Treasury secretary determines that such discrepancy was the product of intentional disregard.

Of note, taxpayers who have made a good faith effort to hire qualified apprentices with respect to the construction of a project are deemed to satisfy the requirement and are eligible for the bonus rate, assuming they have also met the prevailing wage requirement when required. A good faith effort is defined as requesting apprentices and receiving a denial or not receiving a response within five business days.

Next Steps

The Davis-Bacon Act prevailing wage and government-registered apprenticeship requirements apply to projects that begin construction 60 days after the Treasury has published relevant guidance with respect to the requirements. Note that these provisions will be subject to additional clarification, reporting and guidance in forthcoming regulatory actions, which ABC will be engaged in and will notify ABC stakeholders about, as appropriate.

Tax Credit Provisions Concerning Prevailing Wage and Apprenticeship Requirements

Production Tax Credit (Sec. 13101): This provision provides taxpayers the option of a base credit rate of 0.5 cents/kilowatt hour, or a bonus credit rate of 2.5 cents/kilowatt hour (inflation adjusted values) for those facilities that meet the prevailing wage and apprenticeship requirements.

Investment Tax Credit (Sec. 13102): This provisions allows taxpayers to claim a tax credit for the cost of energy property with a base credit rate of 2 or 6% of the basis of energy property or a bonus credit rate of 10 or 30% of the basis of energy property.

Carbon Oxide Sequestration (Sec. 13104): This provision provides a 5X bonus credit rate of $85 per metric ton of carbon oxide captured and sequestered in geological storage and a 5X bonus credit rate of $60 per metric ton of carbon oxide captured and utilized in an enhanced oil recovery project or for a commercial use that results in permanent sequestration.

Zero-emission nuclear power production credit (Sec. 13105): The provision provides a base credit rate of 0.3 cents/kilowatt hour and a bonus credit rate of 1.5 cents/kilowatt hour for electricity produced by the taxpayer and sold to an unrelated person during the taxable year.

Clean hydrogen production credit (Sec. 13204): This provision creates a new tax credit for the production of clean hydrogen. The credit is equal to the applicable percentage of the base rate of $0.60 or the bonus rate of $3.00, indexed to inflation, multiplied by the volume (in kilograms) of clean hydrogen produced by the taxpayer at a qualified facility during the taxable year.

Energy efficient commercial buildings deduction (Sec. 13303): To receive the 5X bonus deduction of $2.50 per square foot, increased by $0.10 per square foot for every percentage point by which designed energy cost savings exceed 25% against the reference standard, not to exceed $5.00 per square foot, taxpayers must satisfy prevailing wage and apprenticeship requirements for the duration of the construction of the project.

New energy efficient home credit (Sec. 13304): To receive a 5X bonus credit of $5,000 for eligible multifamily units certified as a zero energy ready under the Department of Energy Zero Energy Ready Home Program, taxpayers must satisfy prevailing wage requirements for the duration of the construction of such units.

Alternative fuel refueling property credit (Sec. 13404): To receive a 5X bonus credit level of 30% for expenses up to $100,000 for each charging station or refueling pump installed, with respect to eligible property, taxpayers must satisfy prevailing wage requirements for the duration of the construction of such property.

Extension of the Advanced Energy Project Credit (Sec. 13501): To receive a 5X bonus rate of 30%, taxpayers must satisfy the prevailing wage requirements for the establishment, expansion or re-equipping of a manufacturing facility and for five years after the project is placed into service, and satisfy the apprenticeship requirements during the construction of the project

Clean Electricity Production Credit (Sec. 13701) & Clean Electricity Investment Credit (Sec. 13702): Taxpayers who pay wages at not less than local prevailing rates and utilize registered apprenticeship programs are eligible to receive 5X elevated credits of 2.5 cents per kilowatt hour or 30%. The prevailing wage and apprenticeship provisions apply in the same manner as for the section 45 PTC and section 48 ITC.

Clean Fuel Production Credit (Sec. 13704): Taxpayers who pay wages at not less than local prevailing rates and utilize registered apprenticeship programs are eligible for 5X elevated credit rates of $1.00 per gallon ($1.75 in the case of aviation fuel).

Expect additional updates on this topic this year.

If you have questions, please contact Peter Comstock or Ben Brubeck with ABC’s Government Affairs team.

Powered by WPeMatico

{kind=link}